Phase Shifts

Staked ETH ETFs and Regulatory Clarity, Finally

Good morning my tasty friends, I hope you’re all having a wonderful start to your weekend.

There’s quite a bit to snack on in this week’s newsletter. We’ve got the launch of BlackRock’s staked ETH ETF, some market updates, and a fresh trade idea from our friend Greg Magadini at Amberdata.

Before we get started though, some quick color on the market…

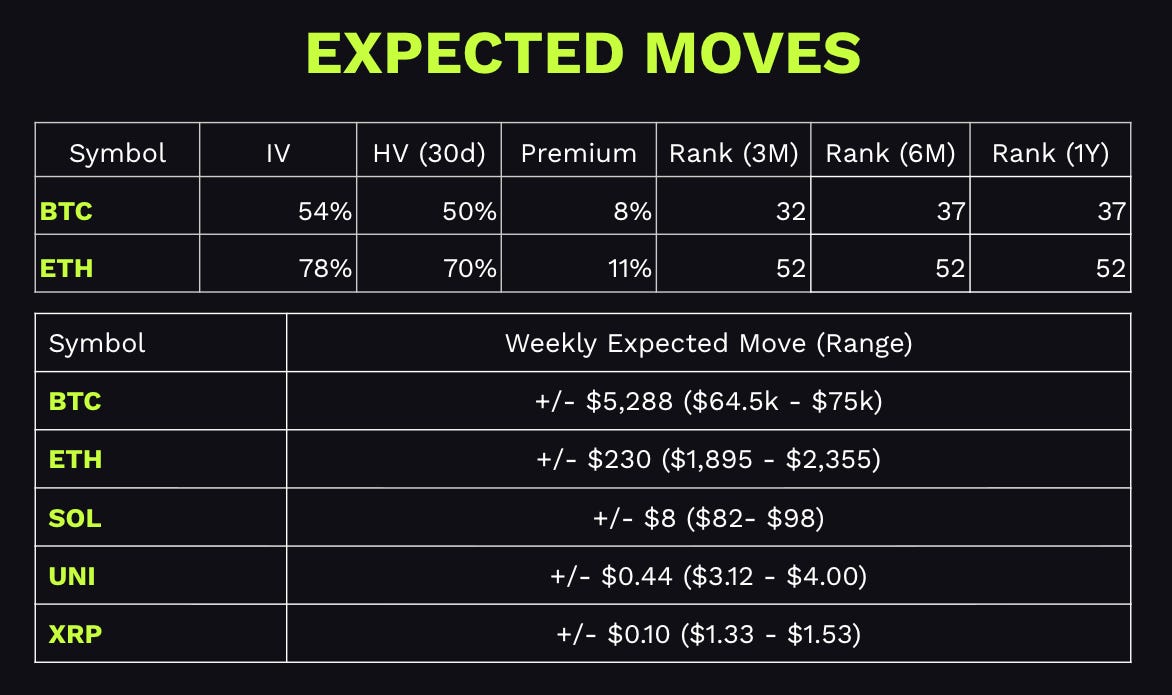

Crypto (BTC, ETH) is showing some signs of stability/resiliency in the face of all the war headlines and market volatility. It’s “trading better” but is still stuck in the multi-month range. Short-term momentum has flipped bullish, but this is within a bearish trend. For the trend to change, we still need to break $79k on BTC, and ETH needs to retake $2,600. Until then, watch, wait, trade the volatility adjusted ranges (see below).

ETH ETFs - Now Staking

BlackRock just launched ETHB, a new ETF that gives investors exposure to both the price of ETH and staking rewards in the form of a monthly dividend. I don’t know how much coverage this has received amidst larger war/geo-political headlines, but it’s a pretty big development, as you can now get ETH price exposure and earn staking rewards through a single ETF.

Before we jump into it, a couple of quick points on staking for anyone that’s not familiar.

Ethereum, and many other blockchains use a consensus mechanism called a proof-of-stake which differs from how Bitcoin and its proof-of-work consensus works. Instead of miners burning electricity to verify transactions like Bitcoin does, ETH uses what are called validators.

Validators lock up their ETH as collateral, that’s the “stake,” and in return, they help process transactions and secure the network. What that actually means is: every 12 seconds, the network picks a validator to propose a new block of transactions. The rest of the validators then vote on whether that block is valid. If consensus is reached, the block gets added to the chain and everyone who participated gets a small reward in newly issued ETH.

For putting their capital at risk and participating in the transaction validation process, validators earn rewards in ETH, and right now, this process yield roughly a 3% annualized return.

Today about 37 million ETH is currently staked, which is roughly 30% of the total supply that’s locked up and earning yield.

That said, it’s not risk free. If you’re a validator and you “misbehave” or go offline, the network can “slash” you, meaning you lose a portion of your staked ETH as a penalty.

Slashing is rare, as there have only been 474 slashing events since Ethereum launched, but the risk isn’t zero. And this matters when we compare ETHB (ETH Staking ETF) with ETHA (ETH Price ETF.)

How ETHB Works

ETHB is BlackRock’s third crypto ETF, after IBIT for Bitcoin and ETHA for Ethereum.

The fund holds spot Ethereum and stakes between 70% and 95% of its holdings through institutional validators operated by the likes of Coinbase Prime, Figment, Galaxy Digital, and others.

The remaining 5% to 30% of its holdings that isn’t staked is what they call the “Liquidity Sleeve.”

The unstaked ETH is held in reserve so the fund can handle redemptions without running into issues from the network’s staking exit queue, which can take days or even weeks to un-stake assets during high-demand periods.

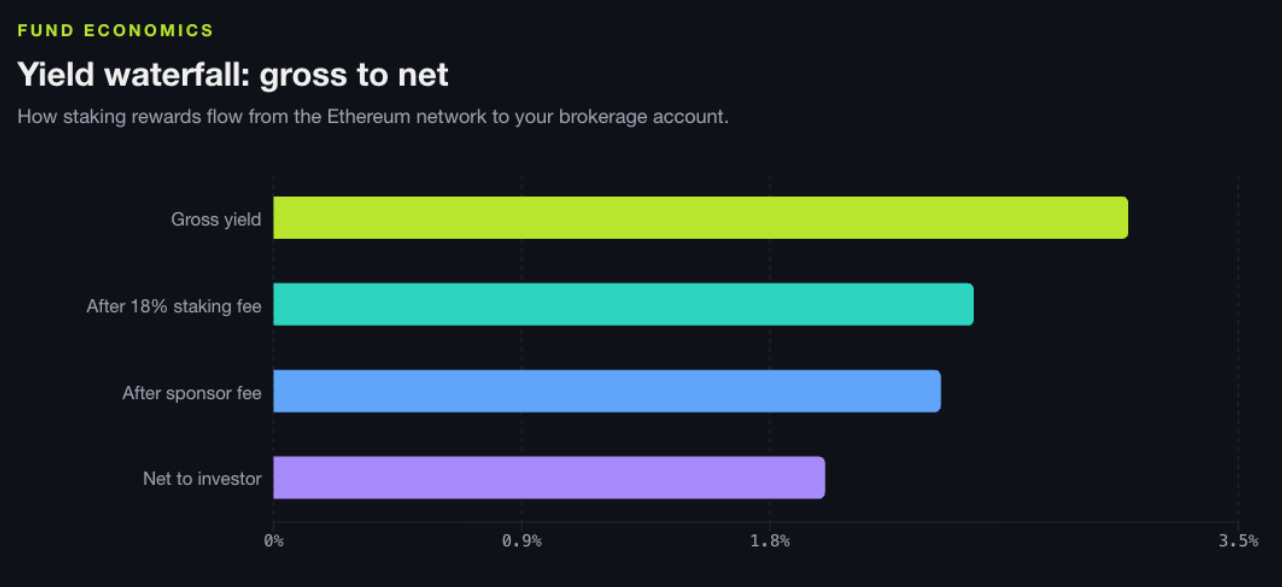

Now, the yield.

Ethereum’s network currently pays about 3% annualized on staked assets. But investors don’t get all of that. BlackRock and its staking providers take an 18% cut of the gross staking rewards as a service fee.

After that fee, and after accounting for the sponsor fee and the liquidity sleeve drag, investors net roughly 1.9% to 2.2% annualized, which is paid out monthly as cash distributions.

Another important detail is that staking rewards are taxed as ordinary income under current IRS guidance. So unlike holding a non-staking ETF where you only deal with capital gains when you sell, ETHB holders will have a tax event every month from those distributions.

Something to keep in mind, especially in a taxable account.

The Regulatory Backstory

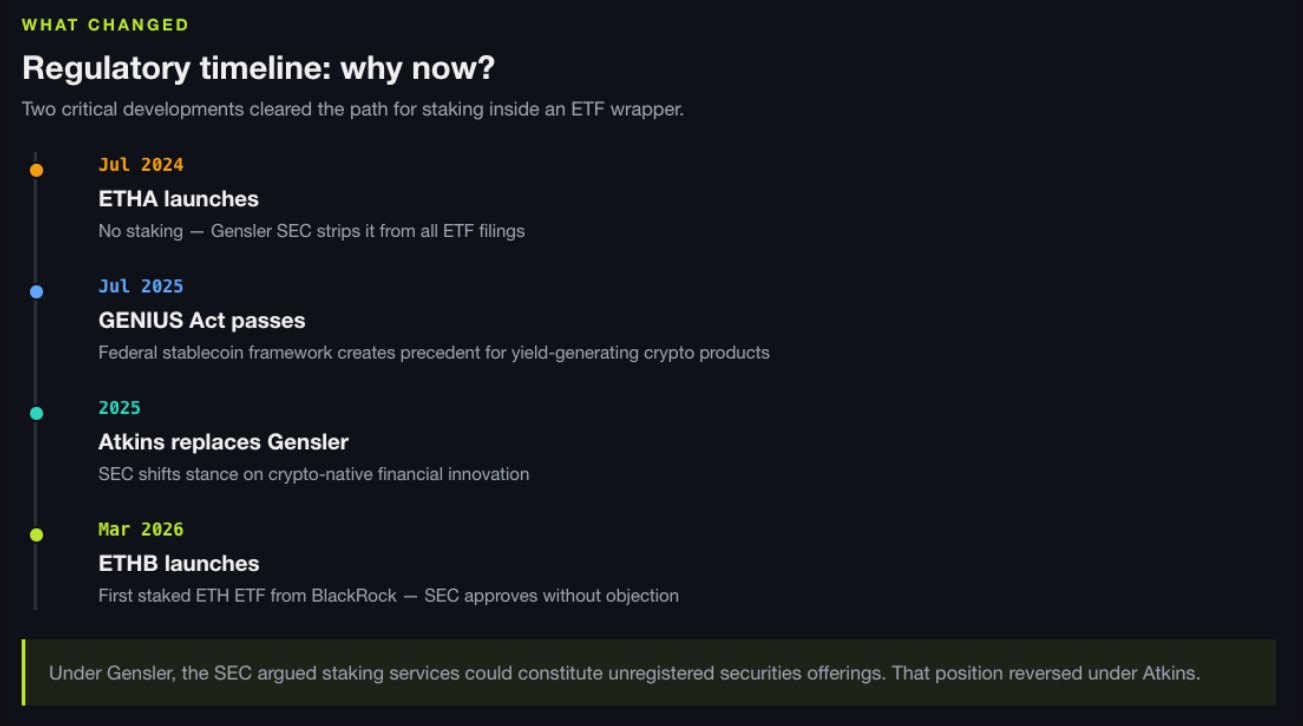

Now you might be wondering… If staking has been around for years, why is this just launching now? Well, it’s largely the result of a major change at the SEC which has led to a significant evolution of the crypto industry in the US.

Under former Chair Gary Gensler, the SEC forced every Ethereum ETF applicant to strip staking from their filings. Gensler’s position was that staking services could constitute unregistered securities offerings. When BlackRock launched its Ethereum ETF, ETHA, in July of 2024, staking was explicitly excluded.

Under current Chair Paul Atkins, this position has reversed, and the SEC approved ETHB’s structure without objection.

Which, doesn’t just open the door for ETHB but potentially opens the door for every proof-of-stake chain to enter the ETF market as a yield-bearing product.

ETHB and ETHA Compared

BlackRock offers two ETH ETFs, ETHA and ETHB. Let’s put them side by side.

ETHA is the straightforward play. You’re getting Ethereum price exposure. There’s no staking, no yield, no additional risk layers aside from ETH price performance. It’s also been around since July 2024, holds $6.5 billion in assets, and it has an active options market. ETHA is also the largest ETH fund in the market.

ETHB is the “upgrade” for total return. It’s the same underlying asset, but with a 2% yield on top of price exposure. The trade-off is you’re taking on slashing risk (which in my opinion is very low), but there is liquidity risk from Ethereum’s staking exit queue, and you’re getting hit with ordinary income taxes on those monthly distributions.

Now why did BlackRock create a separate fund instead of just adding staking to ETHA?

A couple of reasons…

Some investors specifically want to avoid staking risk. Validators can get penalized, staked ETH has exit queue delays, and its generally more complex, even though the staking process is managed by institutional-grade providers. So, keeping them separate lets investors choose the product that matches their risk tolerance.

And there’s some nuance, which doesn’t get enough attention.

Arguably ETHA holders are at a disadvantage over time.

Staking rewards on Ethereum come from newly issued ETH. The staking yield is not generated from external revenue, but is the result of ETH’s inflation dynamic, as the staking reward is essentially a claim on new tokens that dilute non-stakers.

If you’re holding ETH and you’re not staking, you’re not insulated from the dilution that ETHB holders or any ETH stakers are capturing. Which, isn’t massive short term, but over years, can result in a significant performance gap.

Which Fund is Better?

Given the staking yield, is ETHB a better or “smarter” investment than ETHA?

Starting with the bullish ETH investment case. If you plan to hold for years, the math tilts toward ETHB. The 2% staking yield compounds. Over five years, assuming ETH’s price is flat, an ETHB holder would have roughly 10% more total return than an ETHA holder just from staking rewards.

And because non-stakers are being diluted by new token issuance, ETHA holders face this supply headwind.

Here’s the counterargument. If you’re a trader, and not in a position as a long-term investment, ETHA might be the better product. It has $6.5 billion in liquidity, a derivatives market, tighter spreads, and no tax drag from monthly distributions.

For short-term positions, the yield is largely noise, as liquidity and options are more important matter.

There’s also the risk angle.

ETHB introduces slashing risk and staking liquidity risk that ETHA simply doesn’t have. Yes, slashing has been extremely rare, and Yes, BlackRock is using institutional-grade validators. But “rare” isn’t risk free.

For investors who want the cleanest, simplest ETH exposure with zero operational risk layers, ETHA is the better product.

Now, will ETHB overtake ETHA in AUM?

In my view… Probably not in the near term. ETHA has a $6.5 billion head start and established market infrastructure. But, over time I think ETHB will grow to be the larger fund. The yield narrative is just too compelling for advisors and institutional investors.

When a financial advisor is choosing between two ETFs from the same issuer with the same fee, and one of them pays a monthly yield, I think they’re probably going to recommend ETHB to clients.

The Impact Beyond Ethereum

Finally, ETHB isn’t just an Ethereum story. This fund structure creates a template that now applies to every proof-of-stake blockchain. This is a step-change for the crypto industry as previously crypto ETFs were only passive instruments that tracked price, but now they’ve become income-generating products that pay monthly yields similar to stock dividends and bonds coupons.

The Skew Trade: Why Bitcoin’s Downside Is Overpriced and the Upside Is on Sale

This week on tastylive YouTube, Dan Cecilia and Greg Magadini from Amberdata present a trade idea that takes advantage of the gap between what traders are paying for crash protection versus what upside exposure actually costs.

Traders are currently paying a steep premium for downside protection while upside exposure is relatively cheap. The options market is priced for a crash that, based on the derivatives and on-chain data covered in the video, may have already happened.

Check out the episode to learn how to set up the trade.

Another Week of Real Progress

The SEC and CFTF have finally provided some long-awaited answers around security classifications questions.

On Monday, March 17, the pair published a joint 68-page interpretive release that clarifies exactly which crypto assets are securities and which aren't. Something regulators have refused to do for over a decade.

Most crypto assets are not securities. The release establishes a five-category token taxonomy of digital commodities, digital collectibles, digital tools, stablecoins, and digital securities. It also explicitly names 16 assets as digital commodities: Bitcoin, Ethereum, XRP, Solana, Cardano, Dogecoin, Chainlink, Avalanche, Polkadot, Litecoin, Bitcoin Cash, Shiba Inu, Stellar, Hedera, Tezos, and Aptos. Check out the tradable cryptocurrencies at tastytrade.

This should also impact regulatory jurisdiction, since digital commodities fall under CFTC oversight, not the SEC. That's a fundamentally different regulatory relationship, and one that's historically been more constructive for market participants and more amenable to innovation.

This release also clears up questions on staking, mining, and airdrops. It explicitly states that receiving mining rewards, participating in staking, and receiving airdrops of digital commodities are not considered securities transactions.

It’s also interesting to see the interpretation of how digital assets can evolve across classifications. A token sold initially through an ICO with promises of returns is a security, but if its network decentralizes and the token's value is ultimately derived from supply-and-demand dynamics vs centralized management/operations, it might then be viewed as a commodity.

Following this initial paper, SEC Chair Atkins has also indicated a formal rulemaking process is coming "in a week or two" and will include an "innovation exemption" for some crypto firms.

That’s it for this week. Subscribe for more tastycrypto content, and as always… Keep your head on a swivel.

Stay tasty,

Ryan

Trading platform and brokerage: tastytrade

Crypto trade ideas and more content: YouTube

Follow: X

Disclaimer: None of this is to be deemed legal or financial advice of any kind and are solely the opinions of the authors. tastycrypto is provided by tasty Software Solutions, LLC. tasty Software Solutions, LLC is a separate but affiliate company of tastylive, Inc. and tastytrade, Inc. Neither tastylive, Inc. nor tastytrade, Inc. are responsible for the products or services provided by tasty Software Solutions, LLC. Cryptocurrency trading is not suitable for all investors.